Market Commentary

Q3 2018

By almost any measure, the US economy is performing as well as it ever has. The jobless rate fell to 3.8%, the lowest level since 1969, supporting real wage growth and strong consumer spending. Corporate earnings are set to rise 25% this year bolstered by a large tax cut, and business and consumer confidence are at 50-year highs. GDP growth and inflation have moved higher allowing the Fed to continue down the path of monetary policy normalization with little concern of pushing the economy into a recession in the near-term.

While the upcoming mid-term elections have created plenty of heated debate, they are unlikely to negatively impact the markets in the short-term. In fact, stocks have historically done well after mid-terms, presumably due to the removal of uncertainty. And with all the tailwinds mentioned above, this time will likely be no different.

The US economy is poised to grow at above average rates over the next few quarters boosted by fiscal stimulus from both tax cuts and increased deficit spending. Longer-term, growth will moderate as higher interest rates translate into higher debt service costs and tight labor markets produce wage pressures that squeeze profits.

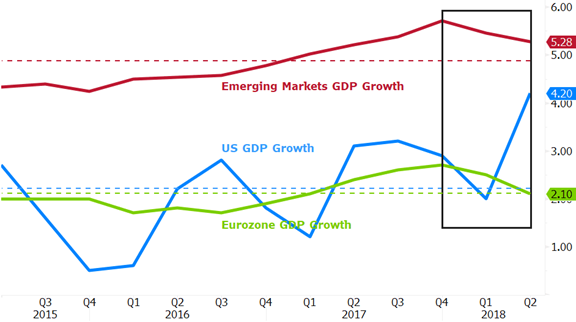

While US growth has gained momentum, economies outside the US have slipped. The graph on the right shows GDP growth rates for three regions: Emerging Markets which is heavily influenced by China (red line), the Eurozone which is heavily influenced by Germany and France (green line), and the US (blue line). Despite the down tick over the past two quarters, Emerging Markets continue to grow significantly faster than Europe and the US. Recently, US growth has accelerated rapidly, while Europe and Emerging Markets have moderated (black box). 4.2% real GDP growth in the US may prove to be the peak, but solid 3% growth is expected for the next 3-4 quarters. That is well above the 2% average (dotted line) that both the US and Europe have experienced over the past few years.

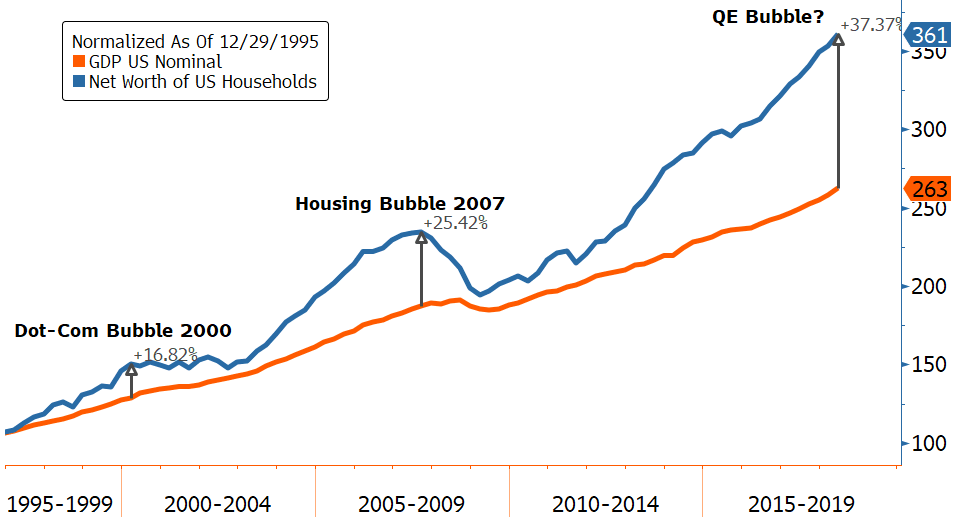

Likelihood of a recession continues to be low in the near-term, but there are underlying risks that must be recognized. The biggest of these is global liquidity which is set to shrink for the first time in 10 years beginning in early next year. The Global Quantitative Easing (QE) that pushed interest rates down to artificially low levels caused asset prices of all types to soar. The accompanying graph shows total US GDP growth (orange line) over the past 25 years relative to US Household Net Worth (blue line). Historically, the two have moved up in tandem, but occasionally they deviate. Note the stability of GDP growth over time and what looks like a minor blip during the 2008-2009 recession. Household net worth on the other hand, tends to inflate and deflate in cycles, adjusting back down to the GDP trendline. The concern today is that asset values are high relative to the size of the economy considering their historical relationship.

US net worth is an aggregate of all assets (stocks, real estate, etc.) minus liabilities (mortgage debt, car loans, credit card and student loans) held by Americans. Net worth has expanded greatly over the past few years and cheap borrowing costs may be partly responsible. For the four years prior to the 2000 peak of the Dot-Com Bubble, net worth expanded almost 17% above the GDP line, but consolidated back as stock values declined over a painful 3-year bear market. From 2003 to 2008, home prices surged and, with help from lower interest rates and lenient lending standards, aggregate net worth again grew above GDP trendline, this time by 25%. The collapse in home prices and equites was historic and, naturally, central bankers did all they could to alleviate the pain.

The emergency measures adopted by the Federal Reserve and other central banks in 2008 went beyond orthodox monetary policy of lowering short-term interest rates adding quantitative easing (QE), which was designed to flood markets with liquidity to more quickly lower long-term interest rates. These extreme measures worked, putting an immediate floor on asset prices and setting the stage for a powerful recovery. Ten years later, it is evident that these measures have pushed valuations for most types of assets above historical levels. As QE turns to QT (tightening), long-term interest rates are set to increase. 10-year US Treasury yields have just hit their highest level in 7 years although, at 3.18%, still low by historical standards and relative to inflation, and are expected to go higher. Despite eight rate hikes over the past two years, US monetary policy is still not considered tight, a testament to just how much monetary stimulus was added and how far the Fed needs to go to get back to “normal”.

Government spending is too high and going higher, increasing 8% next year, a level that is more than double GDP growth and clearly unsustainable. Roughly 20% of the federal budget must be financed every year due to overspending. This is a risk that will eventually be recognized as more and more debt is added and interest costs balloon as a percentage of the deficit.

Tariffs are another risk to growth. They are currently being used as a tool by the Trump Administration to bring trading partners to the negotiating table. By allowing other counties to maintain higher tariffs for many decades while continuing to consume their goods, we’ve subsidized growth and improved standards of living around the globe. New tariffs may hamper growth in certain industries, however, the impact is small relative to the overall economy and to the current size of fiscal stimulus. As we just saw with the re-negotiation of NAFTA, we expect a positive result from talks with Europe and China, ultimately bringing global tariffs down and relieving some of the pressure on stocks outside the US which have underperformed this year.

3rd Quarter 2018 Performance

Stocks

- Stocks globally were up (↑4.4%) led by US Large, Mid and Small Caps (↑7.5%, ↑5.7%, and ↑3.8%, respectively) followed by underperforming Non-US stocks (International Developed (↑1.4%), International Small Cap (↓2.5%), and Emerging Markets (↓0.7%). Non-US equities were primarily hurt by the rising US Dollar.

- Looking ahead, US earnings reports continue to be strong, which should provide support for stocks. Non-US stocks continue to be hurt by trade war fears.

Bonds

- Total returns for broad market bonds were down slightly (↓.08%) as interest rates climbed higher. Municipals, Floating Rate Bank Loans, and High Yield Corporates also had mixed performance (↓0.38%, ↑1.47%, and ↑3.0%, respectively).

- Looking forward, higher interest rates mean more attractive reinvestment opportunities but lower prices on existing bonds.

Alternatives

- The Alternatives portfolio turned in positive performance for the quarter (↑1.70%). Hedged Equity (↑2.8%), Market Neutral (↑0.3%), Managed Futures (↓1.4%) and Multi Strategy (↑1.0%).

- Alternatives performed better than bonds during the quarter with similar risk. We expect the two primary performance headwinds, value underperformance and the strong US Dollar, to reverse in the near-term.

![]()

Royce W. Medlin, CFA, CAIA

Chief Investment Officer